UK audit exemption rules determine whether your company needs a statutory audit or can file unaudited accounts. The rules sit in the Companies Act 2006, and they’re more involved than most directors expect – particularly for group structures, subsidiary undertakings and businesses approaching the thresholds. Get the claim wrong and Companies House can reject your filing. Get it right and you could save thousands in fees each year.

This guide covers the specific mechanics: who qualifies, the two-year consecutive test, how subsidiaries claim relief through a parent’s guarantee, and which entities can never be exempt from audit.

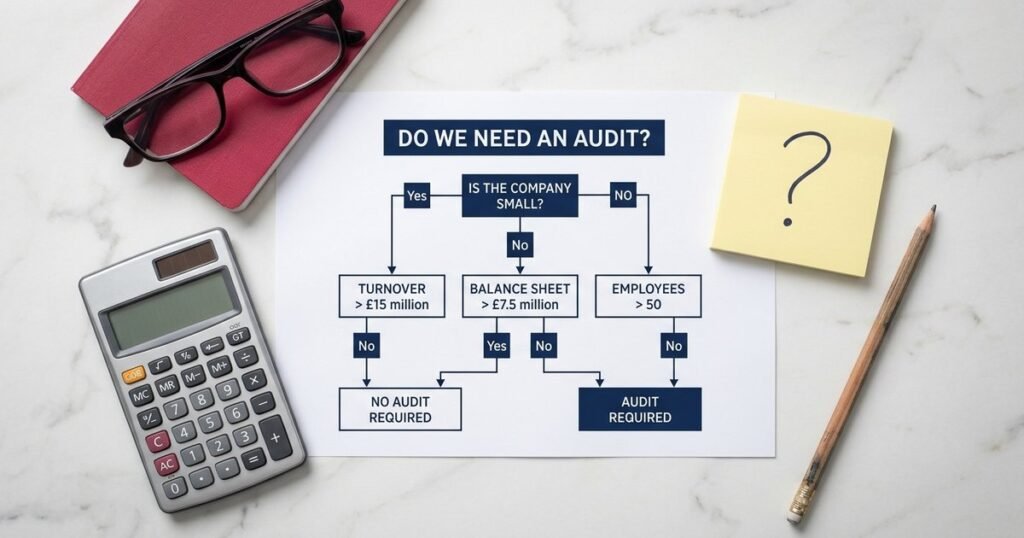

Who is eligible for audit exemption in the UK?

A private limited company can claim audit exemption if it qualifies as small under the Act. To qualify as small, the company must meet at least two of three conditions in a given financial year:

- Annual turnover not exceeding £15 million

- Balance sheet total not exceeding £7.5 million

- Average number of employees not exceeding 50

These figures apply to financial years starting on or after 6 April 2025. Before that date, the old limits applied (£10.2m turnover, £5.1m balance sheet, 50 employees). The threshold changes were the first increase since 2016 and brought around 13,000 additional small companies into scope for relief.

But meeting two out of three isn’t enough on its own. The company also needs to pass some other tests. It can’t be a public company. It can’t be a banking company or an authorised insurance company. And it can’t be a traded company with shares on a regulated market. Small companies that tick those boxes are eligible – everyone else needs to look at the exceptions more carefully.

What is the 2-year rule for audit exemption?

You don’t qualify based on a single financial year. The Companies Act 2006 requires companies to meet the small company thresholds for two consecutive years before they can claim relief. Directors sometimes miss this – a company that dips below the limits in year one but was above them in the previous year still needs an audit for that first year.

The flip side works in your favour too. If your company has been small for years and then breaches the thresholds in one financial year, you don’t lose your status immediately. You keep it for that year and only require an audit from the following year if you breach again. It’s a buffer that stops companies bouncing in and out of audit every time turnover fluctuates.

There’s one exception: a newly incorporated company. In its first financial year, it only needs to meet the tests once. There’s no prior year to compare against, so a single qualifying year is enough.

Practical tip – review your position against the size thresholds annually. Growth, acquisitions, or even inflation pushing up your balance sheet total can shift you across the line. And once you need an audit, you must appoint a registered auditor before your accounts are due.

How do group companies and subsidiaries claim exemption?

Group structures are where audit exemption gets complicated. There are two separate routes, and they work differently.

Small group exemption

If a company is a member of a group, the group itself must also qualify as small for the individual entities within it to claim relief. The group thresholds mirror the individual ones but are applied on a consolidated basis:

- Aggregate turnover not exceeding £15 million net (£18 million gross)

- Aggregate balance sheet not exceeding £7.5 million net (£9 million gross)

- No more than 50 employees across the group

A subsidiary company might individually be tiny – say, £500,000 turnover with three staff. But if its parent runs a £20 million group, that subsidiary can’t use the small company route. The group fails the test, and individual size doesn’t matter.

This catches out a lot of UK companies with overseas parents. If the worldwide group is large, the UK subsidiaries within it generally need auditing unless they can use the s479A route below.

Subsidiary exemption under s479A

Section 479A of the Companies Act 2006 provides a separate exemption from audit for subsidiary companies – even those in large groups. The conditions are specific:

- The UK parent (or EEA-established parent) must give a statutory guarantee over all the subsidiary’s liabilities for that financial year

- All shareholders of the subsidiary must consent – unanimously, not by majority vote

- The parent must prepare and file consolidated group accounts that include the subsidiary

- The subsidiary must disclose the guarantee in the notes to its own accounts

This parent guarantee is a real legal commitment, not a formality. If the subsidiary can’t pay its debts, the parent is on the hook. Some parent companies are reluctant to give this for trading subsidiaries with significant liabilities. But for dormant holding companies, property vehicles, and management company entities within a group, it’s a common and practical route.

One important restriction: the subsidiary itself can’t be an entity that’s ineligible. A banking subsidiary or traded subsidiary still needs its own audit even with a guarantee in place.

Which companies can never claim audit exemption?

The Act lists several categories of company that can never qualify for relief, no matter how small they are. These are sometimes called “ineligible entities” (and when they form part of a structure, the whole thing can become an ineligible group).

Companies that always need an audit include:

- Public companies – every PLC needs an audit, whether traded or not

- Traded companies – any company with securities admitted to a UK or EU regulated market

- Banking companies and e-money issuers

- Authorised insurance companies and Lloyd’s managing agents

- UCITS management companies and MiFID investment firms

- Companies in an ineligible group – if any member falls into the categories above, the group is ineligible and other entities lose their relief route via the small group test

There’s also the shareholder override. Under s476 of the Act, shareholders holding at least 10% of issued share capital (or 10% of any class of shares) can demand an audit by written notice. The directors can’t refuse. This comes up regularly in joint ventures and businesses with minority investors who want independent assurance over the accounts.

What happens if you get the exemption wrong?

Filing unaudited accounts when your company should have had an audit is a criminal offence for directors under the Act. The registrar can reject the filing outright, which triggers late filing penalties – up to £7,500 for private companies if accounts end up more than 12 months overdue.

Beyond penalties, getting it wrong damages credibility. Banks doing due diligence will notice. Potential acquirers doing pre-sale checks will flag it. And HMRC sometimes takes an interest in companies that have incorrectly claimed relief, particularly where there’s a complex group structure.

If you discover you’ve wrongly claimed in a prior year, take advice quickly. It’s usually possible to rectify the position by filing amended accounts with an audit report, but acting fast limits the fallout.

When a voluntary audit makes sense

Some UK companies that clearly qualify for relief still choose to have an audit. A voluntary audit is common where lenders require audited accounts as a condition of funding, or where multiple shareholders want independent oversight. It’s also worth considering before a sale – buyers nearly always want audited financial statements, and having them ready speeds up the process.

The cost of a voluntary audit for a company below the threshold is typically between £3,000 and £10,000 depending on complexity. For some businesses, that’s a worthwhile investment in governance and stakeholder confidence.

Get clarity on your audit position

The rules interact with group structures, shareholder rights, regulatory status, and the two-year qualifying period in ways that aren’t always obvious. If you’re unsure whether your company genuinely qualifies – or if you’ve just crossed the thresholds and need to appoint an auditor for the first time – we can give you a straight answer.

Audit Group is part of Jack Ross Chartered Accountants, ICAEW-regulated and based in Manchester. We advise on statutory audit obligations for businesses across the UK.

Call us on 0161 832 4451 or get in touch online.