An audit trail is a chronological record of every transaction, change or event within a system, from start to finish. Think of it as a paper trail, but digital. Every entry, approval, edit and deletion gets logged with a timestamp and user ID, so you can trace exactly what happened, when it happened and who did it.

For UK businesses subject to statutory audit, a well-maintained audit trail is not optional. It’s how your auditor verifies that the numbers in your financial statements match reality. And when things go wrong, it’s how regulators piece together what happened.

What is meant by audit trail?

An audit trail is a sequential log that tracks activities through a system. In accounting, it connects source documents (invoices, receipts, bank statements) to the entries in your general ledger and ultimately to the published financial statements. The trail works both ways: an auditor can start with a figure in the accounts and trace it back to the original document, or start with a transaction and follow it through to the financial statements.

The term also applies more broadly. IT audit trails log system access, configuration changes and data modifications. Compliance audit trails record when policies were reviewed and by whom. But the core idea is always the same: an unbroken chain of evidence showing what happened.

What does an audit trail do?

An audit trail serves three practical purposes:

- Verification. Your auditor uses the trail to confirm that transactions are real, complete and recorded in the right period. Without it, they can’t form an opinion on your financial statements.

- Accountability. The trail shows who authorised each transaction. If a payment was made without proper approval, the audit log makes that visible.

- Detection. Unusual patterns in the audit trail – duplicate entries, transactions at odd hours, changes to completed records – can flag errors or fraud before they cause serious damage.

In practice, the audit trail helps companies catch mistakes early. A missing purchase order, an invoice recorded in the wrong month, a journal posted without supporting documentation – all of these show up when the trail is reviewed properly.

Types of audit trails

Different types of audit trails exist because different systems need different kinds of tracking.

Financial audit trails

The most common type in a business context. This tracks every financial transaction from its source document through to the financial statements. Your accounting software should generate this automatically – every journal entry, every bank reconciliation, every adjustment gets logged with a date, amount, account code and user ID.

IT and system audit trails

Also called audit logs or access logs. These record who logged into a system, what they accessed, what they changed, and when. They’re essential for data security and for meeting GDPR requirements around personal data access. If your company stores customer data, regulators expect you to know who accessed it and why.

Compliance audit trails

These document how your organisation meets its regulatory requirements. For example, a company regulated by the FCA would maintain trails showing when compliance policies were reviewed, when staff training was completed, and how customer complaints were handled. The trail proves you followed the process, not just that you had one.

Operational audit trails

These track changes to business processes, approvals of procurement decisions, and modifications to standard procedures. They’re less about financial accuracy and more about operational efficiency and governance.

Why are audit trails important?

Audit trails matter because they create transparency. And transparency is what auditors, regulators and investors all demand.

For statutory audit purposes, an incomplete audit trail creates real problems. If your auditor can’t trace a balance back to its source, they may need to qualify their opinion or issue a limitation of scope. That’s a red flag for lenders, investors and Companies House.

Beyond compliance, audit trails also help with:

- Fraud prevention. The knowledge that every action is logged acts as a deterrent. And when fraud does occur, the trail provides the evidence needed for investigation and recovery.

- Data integrity. Audit trails catch data entry errors, duplicate transactions and unauthorised modifications before they compound into material misstatements.

- Regulatory compliance. UK companies must comply with the Companies Act 2006 requirement to maintain adequate accounting records. The audit trail is how you demonstrate that. GDPR adds further requirements around logging access to personal data.

- Dispute resolution. When there’s a disagreement about what was agreed or what was delivered, the audit trail provides objective evidence.

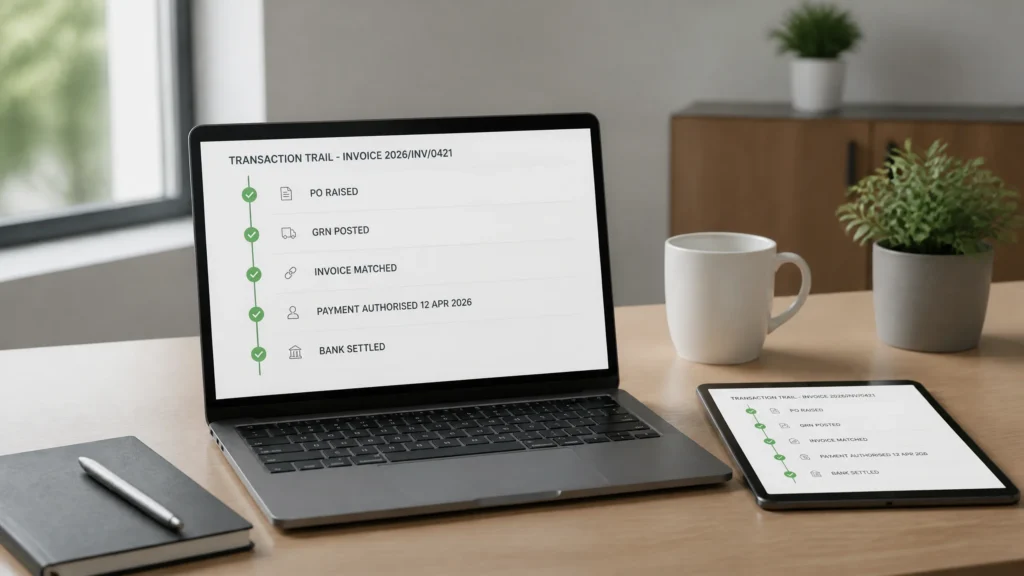

What is an example of an audit trail?

Here’s a simple example. Your company buys office furniture for £2,400.

- An employee submits a purchase requisition (logged in the procurement system)

- A manager approves the purchase (approval logged with timestamp)

- A purchase order is sent to the supplier (PO number recorded)

- The furniture arrives and a goods received note is completed

- The supplier sends an invoice, which is matched to the PO and GRN

- The accounts team posts the invoice to the fixed assets account in the general ledger

- Payment is made via bank transfer (bank reference recorded)

- The asset is added to the fixed asset register with a depreciation schedule

Each step in that chain is documented. Your auditor can start at any point and trace the transaction forwards or backwards. That’s the audit trail in action.

Best practices for maintaining audit trails

A good audit trail doesn’t happen by accident. It requires consistent processes and the right tools.

Use accounting software with built-in logging

Modern cloud accounting packages (Xero, Sage, QuickBooks) automatically maintain audit logs. Every entry is timestamped and linked to a user. Manual spreadsheets don’t provide this level of tracking, which is why auditors always prefer system-generated records.

Don’t delete or overwrite records

If an entry is wrong, post a correcting journal rather than editing or deleting the original. The original entry and the correction should both be visible in the trail. Deleted records create gaps that your auditor will question.

Attach source documents

Scan and attach invoices, contracts and approvals to the corresponding ledger entries. This makes the trail self-contained – your auditor won’t need to request boxes of paper files.

Review the trail regularly

Don’t wait for the annual audit. Monthly reviews of the audit log can catch errors and unauthorised changes early. This is especially important for businesses handling high transaction volumes.

Control user access

Limit who can post journal entries, approve payments and modify records. Segregation of duties is a core internal control, and the audit trail should reflect it. If one person can create a supplier, raise a PO and approve the payment, that’s a control weakness your auditor will flag.

Automated audit trails

Automation removes the biggest risk to audit trail integrity: human error. When records are created manually, steps get skipped, documents get lost and entries get posted to the wrong accounts.

An automated audit trail captures every event as it happens, without relying on someone to remember to log it. Workflow tools can enforce approval sequences (no payment without sign-off), and accounting software can prevent journals from being posted without supporting documentation attached.

For UK businesses preparing for their first statutory audit, investing in good accounting software with proper audit trail functionality is one of the most practical steps you can take. It reduces your audit fees (because the auditor spends less time chasing documents) and it reduces the risk of audit adjustments.

Audit trail requirements in the UK

UK companies face several regulatory requirements around record-keeping and audit trails:

- Companies Act 2006, Section 386 requires every company to keep adequate accounting records that show and explain the company’s transactions, and that are sufficient to enable the directors to prepare accounts that give a true and fair view.

- GDPR requires organisations to log access to personal data and to be able to demonstrate compliance with data protection principles.

- ISA (UK) 230 sets out the auditor’s responsibility for audit documentation – but it also means your auditor expects you to have documentation they can review.

- HMRC requires businesses to keep records for at least 6 years (5 years for self-assessment). The audit trail is how you substantiate your tax returns if questioned.

For regulated industries, additional requirements apply. Solicitors must maintain detailed client account records for SRA audits. Charities above the audit threshold need records that satisfy Charity Commission requirements. Financial services firms must meet FCA record-keeping standards.

Related reading

- The Audit Process: A Step-by-Step Overview

- Audit Adjustments Explained

- Material Misstatement in Audit

- Audit Findings: The 5 Elements

How Audit Group can help

If you’re not sure whether your audit trail meets the standard your auditor will expect, we can help. Our team reviews hundreds of audit trails every year and we know exactly where businesses tend to fall short. We’ll assess your current systems, flag any gaps, and work with your finance team to get things right before the audit starts.

Request a proposal or call us on 0161 832 4451 to discuss your audit requirements.